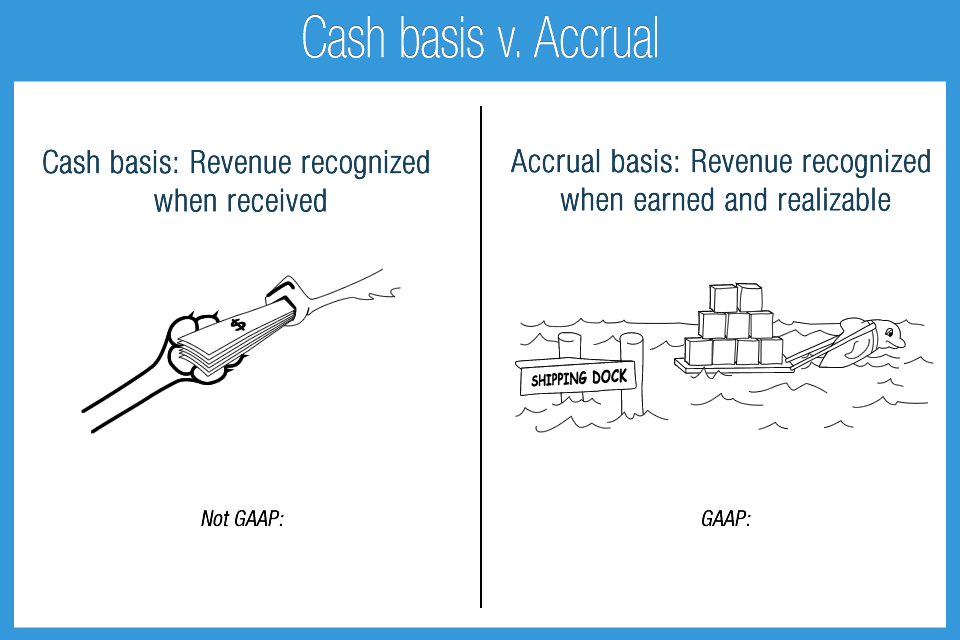

Cash basis v. Accrual: The cash basis method of accounting recognizes transactions only when cash or equivalents have been exchanged. Accrual basis follows the matching principle and records (recognizes) transactions as they occur

- Only accrual basis accounting is an acceptable method under Generally Accepted Accounting Principles US

- Cash basis records revenue and expenses only when cash or equivalents have been exchanged

- Accrual basis records revenue when earned and realizable and expenses as incurred, even if cash has not been paid