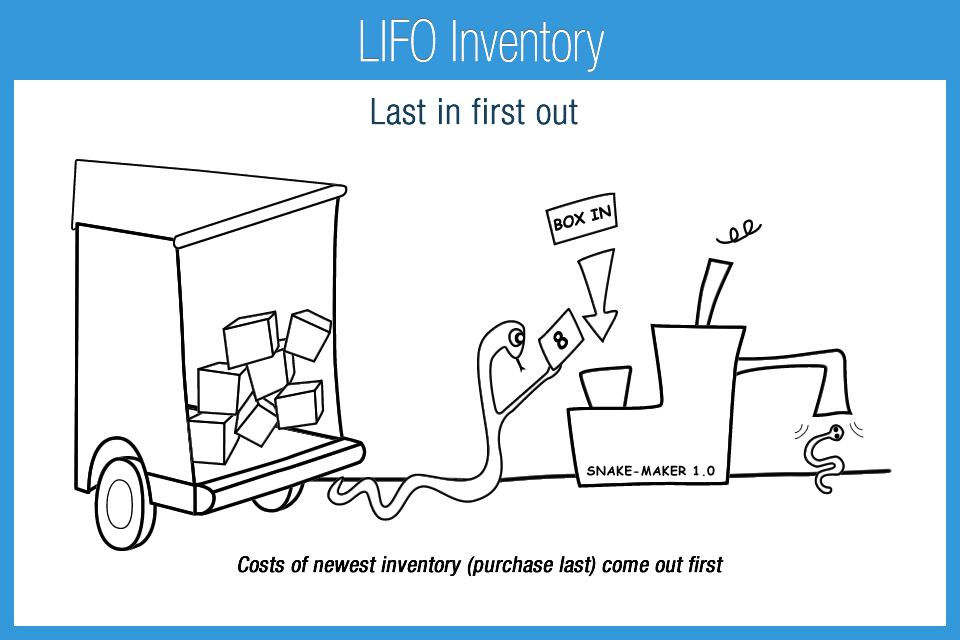

Last in first out: Inventory accounting system in which last purchases are the first to be used to determine ending inventory and the cost of goods sold

- Oldest costs tend to remain in the inventory account

- Results in lower net income in a period of rising prices when compared to the FIFO method

- Inventory value is understated in period of rising prices

- Acceptable method only under GAAP